Experiential is the saviour of the high street. I feel like I’ve been hearing that for years. But as 2018 continues to hand out death certificates to big-names, it’s hail Mary time. Brands need to hear the message or there won’t be a later.

Some retailers are waving flags and making hay with experiential as the stragglers drown in obligations from a bygone era. In retail, as in life, the past is gone; the future is here and it’s evolving all the time.

The irreversible change in behaviour

When my phone chimes, my brain’s pleasure zone ignites; the same bit that responds to drugs and gambling. Dopamine flows. My arm starts to jitter and … BAM! No time to think before I autograb the phone to see who wants a piece. Maybe you’re the same.

Psychologically, consciously, unconsciously, our brains and bodies are responding to the tech takeover: we’re being subtly, constantly, irreversibly upgraded. And as my generation willingly recodes its behaviours, the age brackets coming up next are being hard-wired with hugely different priorities.

When I hear that technology is killing the high street, I have to laugh. Technology is ready and waiting to enable, empower and evolve retail. But merchants, on the whole, are trapped.

Big retailers are stuck between two worlds. There’s a past and a future. The legislative framework, shareholder expectations and shops’ commercial structures and obligations belong in the past while shoppers’ behaviours hail from the future. There is an online world which makes great fiscal sense and an offline one that doesn’t. Prime retail on Main Street isn’t any longer efficient. Ranking on Google is.

We’re seeing fantastic examples of online-first businesses cherrypicking the best of bricks and mortar to add a showrooming/ experiential dimension to their brand. Concepts that aren’t about direct retail; that are about something else. When brands – from indies to big-hitters, conglomerates to local cafes – score a high street success, customers buying stuff is often secondary to the experience of it all.*

But the merchants and brands behind gimmick, gallery or concept store initiatives are outliers: a minority that have written a business case to justify often loss-leading bricks and mortar activity to support bigger online objectives. For the majority, physical retail is the status quo. And it’s cumbersome, stale, unfair and illogical.

Retailers’ losing battle

Under current rules and shareholder expectations, the onus is on retailers to turn around their own container ships (yes many have to accept blame for not traversing the iceberg earlier) and invest in the right stock, tech, infrastructure, supply chain and messaging. But they’re using instruments of today to retroactively deconstruct an amorphous, solid concrete fossil.

Stores that set up online and draft bricks and mortar in later give themselves the best of both worlds. Legacy retailers are hungover. Their business models cannot be moved piecemeal into a new era – the digital switchover, read experiential, has to happen now.

The mandate for evolution is in and it’s codified in bits and bytes. We are not about to revisit the behavioural staples of the past. The high street can’t expect that yesterday’s habits will suddenly snap back into place. The opposite is happening and demographic attrition will continue to obliterate the mould.

How many more retail corpses?

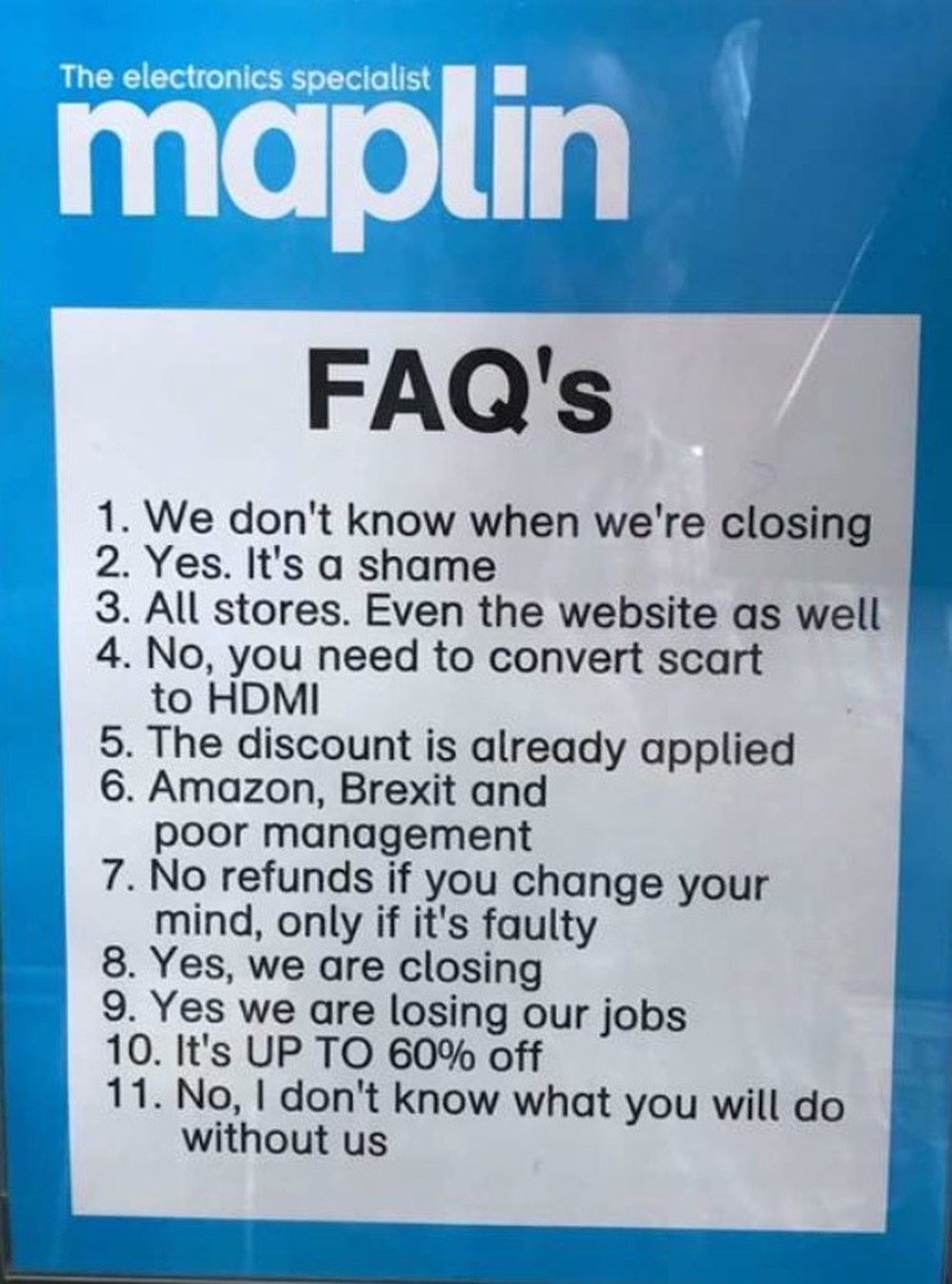

The year 2018 has been something of a wake-up call. Time was called on Maplin and Toys R Us, with various others circling the drain. House of Fraser will close 30 stores – including its flagship Oxford Street branch – while the likes of Marks and Spencer, Debenhams, Mothercare, Carphone Warehouse and New Look are rebooting to stay in the game.

Last year nearly 6,000 shops closed on UK high streets, including 1,700 chain stores. An average of 11 stores per day opened, while 16 per day closed. It’s said that the UK high street is in a poorer condition now than in 2008, at the height of recession.

We hear a lot about the suffering. And no one wants to minimise or denigrate the ramifications of mass store closures on people’s jobs, lives and communities.

But not enough plaudits are handed down to the innovators, those who are making a real statement with their experiential high street activity. The notion that we need healthy shops on the high street is perpetuated by habit. Yet a richer future may await if we redefine ‘healthy’ to mean vibrancy, footfall and people instead of profit.

Lessons from online

The values of the online world are many. We’ve become obsessed with making what works in the physical world translate better and cheaper in an online environment. But forward-thinking brands are more intent on the reverse: bringing activity offline after testing and conceptualising it online.

Better still, they’re using the best of offline to fill gaps where online doesn’t make the grade. So often the opposite is the obsession.

In online we value engagement, impressions, joining up experiences, flawless customer journeys, serving great content for free. We ascribe an intangible value to experience that we don’t measure directly in pounds and pence. Brands need to earn and reward people’s attention without a discernible transaction taking place.

Borrowing those principles for the physical world and we can create infinitely more opportunities to stir emotional, spiritual, educational, familial transactions that mightn’t payoff on the balance sheet, but do drive value for the collective whole.

It’s cliché time, but instant gratification; a hunger for experience; an always-on lifestyle; up-for-grabs-loyalty. The combination of these factors, and inexhaustible others, have created a wildly different retail climate than the one in which our high street staples originally set up shop.

But beneath the doomsday headlines, the high street is swimming in hope. Over 80% of all transactions still happen there. As devoted as we all are to our smartphones, the trends still point at a shopperbase that lusts after a physical, human experience, even above price. And when in-store and mobile are combined in some way, conversion rates spring 20%.

Experience a new hope

Bill Grimsey, author of The Vanishing High Street called for retail to ‘recapture a sense of vibrancy, social cohesion and face-to-face encounters’, while Forbes identified six measures of experiential retail: It must be intuitive, human, meaningful, immersive, accessible and personal.

Tech has ultimately redefined what a transaction is. Return-on-investment has evolved to return-on-engagement. Let’s see physical run with the baton. Do we really need pounds and pence if the aim of the game is to enrich people in ways beyond Sterling?

People know where to shop: online. What can’t people get online? Community, experience, human contact, new physical and emotional possibilities.

What’s the high street for again?

*****

Online has also bred more and more creative and subtle iterations of the Call – to – Action. But this time we’re going old fashioned:

If you’re stuck on the high street, with no idea which way to go or how to strategise how experiential can work for you, come and say hello. Our talented indie network is bursting with creativity, fresh ideas and the metrics upon which we can convert your dot problems what into dot change.

*****

*Innovative retail concepts

Rough Trade Records has evolved. With its coffee shop, live gigs and signings fans can access a multi-dimensional music experience, for a nominal charge, alongside their fellows.

Virgin Holidays, like many in the sector, uses VR to bring customers closer to its intangible product and enrich the consideration experience.

Topshop brought the catwalk into its stores for London Fashion Week. Visitors to the store could don an Oculus Rift headset and be transported to the front row.

The new Sonos 101G store in New York recreates an acoustically perfect house via seven separate booths, encouraging shoppers to relax and hang out while listening to music.

Lidl surprises – rotating inventory so customers never know exactly what they’ll get (in the middle aisles).

The House of Vans has become a hub for skaters with a live music stage, skate park, art gallery, café, bars and cinema.

Nike Town is one of the homes and meeting points of Nike Running Club, a free club for city runners looking to meet new people.

The Rapha store is a great place to hang out for cyclists with its Italian café vibe, a casual browse amongst its offerings doesn’t feel like shopping in the slightest.

High-end US athleisure wear brand Lululemon lets customers buy new workout gear and attend a yoga class in store.

From soap to salad to chocolate boxes, DIY shopping experiences play well. With Lush there’s that, and an added dose of ecopolitics which, like it or not, is steadfastly sure what it is and what it stands for.

Budget fashion retailer Primark now accounts for one in seven clothing items sold in British shops and it doesn’t even have an online offering. Despite no dotcom infrastructure, Primark’s share of the UK clothing market has grown from 15% to 16.5% with revenues edged up to £7.1 billion and £735 million in profit.

As well as stocking 450 designer brands, including Balenciaga, Gucci, Saint Laurent, Prada, Valentino, Alexander McQueen, not only is luxury fashion house MatchesFashion moving into its own private labels, 95% of its revenue is generated online but three London stores and a private townhouse enable clients to experience luxury, private shopping, events and more.

MatchesFashion reported revenues of £204 million in 2016, a 61% jump.

Furniture businesses Made.com, Loaf and Oak Furniture Land all trade mostly online. But all three offer physical showroom space to complement and conceptualise its online inventory. Oak Furniture Land grew its UK showroom presence to 100 locations. Turnover soared to £279.7 million from £239.3 million the year before.

The list goes on.